Car Loan Pre-Approval: Why It Matters and How to Get It

Car FinanceIf you're planning to buy a car soon, one of the smartest moves you can make is getting pre-approved for a car loan. It’s like walking into the dealership with a VIP pass — you already know your budget, your rate, and your negotiating power. Let’s explore why pre-approval matters in 2025 and how to get it step by step.

1. What is car loan pre-approval?

A pre-approval is when a lender reviews your financial details — like credit score, income, and debt — and gives you a conditional offer for a loan. It tells you how much you can borrow, your estimated interest rate, and your monthly payment range.

With the Life Planner app, you can easily track your pre-approval offers using its Loan Tracking and Amortization Tools. You can compare lender terms side by side, calculate how much interest you’ll pay over time, and store every detail securely.

2. Why pre-approval matters

- Know your budget: You’ll shop confidently, knowing what you can afford before you step onto the lot.

- Lock in your rate: Many lenders hold your rate for 30–60 days, protecting you if rates rise.

- Gain leverage: Dealers take you more seriously when you already have financing ready — you’re negotiating as a cash buyer.

- Avoid surprises: You’ll know your credit situation upfront and can fix issues before applying formally.

3. How to get pre-approved

It’s simpler than most people think. Here’s the quick route:

- Check your credit score and clean up any errors.

- Gather documents like income proof, ID, and address verification.

- Apply with multiple lenders online — most soft-pull inquiries won’t affect your credit.

- Compare your pre-approval letters carefully for rates, loan terms, and conditions.

You can use the Expense Tracker and Budgeting Tools inside Life Planner to organize your monthly expenses before applying. This helps you figure out how much of a car payment fits comfortably into your lifestyle.

4. How Life Planner helps during the process

Life Planner isn’t just about numbers — it helps you build the consistency and mindset to manage debt responsibly. Use the Habit Tracker to schedule reminders for checking your credit, saving for a down payment, or comparing new offers. The Habit Calendar and Progress Tracking features make it easy to stay on track.

Buying a car can be emotional, too. That’s where the Mood Tracker and Mood Journal come in handy — helping you understand how money decisions impact your stress or excitement levels so you can make balanced choices.

5. Once you’re approved — plan ahead

When you finally get your pre-approval, don’t rush! Use it to guide your car shopping within budget. Enter your estimated loan details in Life Planner’s Loan Amortization tool to visualize how payments will look month to month, and use the Financial Reports feature to see how your car fits into your bigger financial picture.

The key takeaway: pre-approval gives you power, confidence, and clarity — all before you set foot in the showroom.

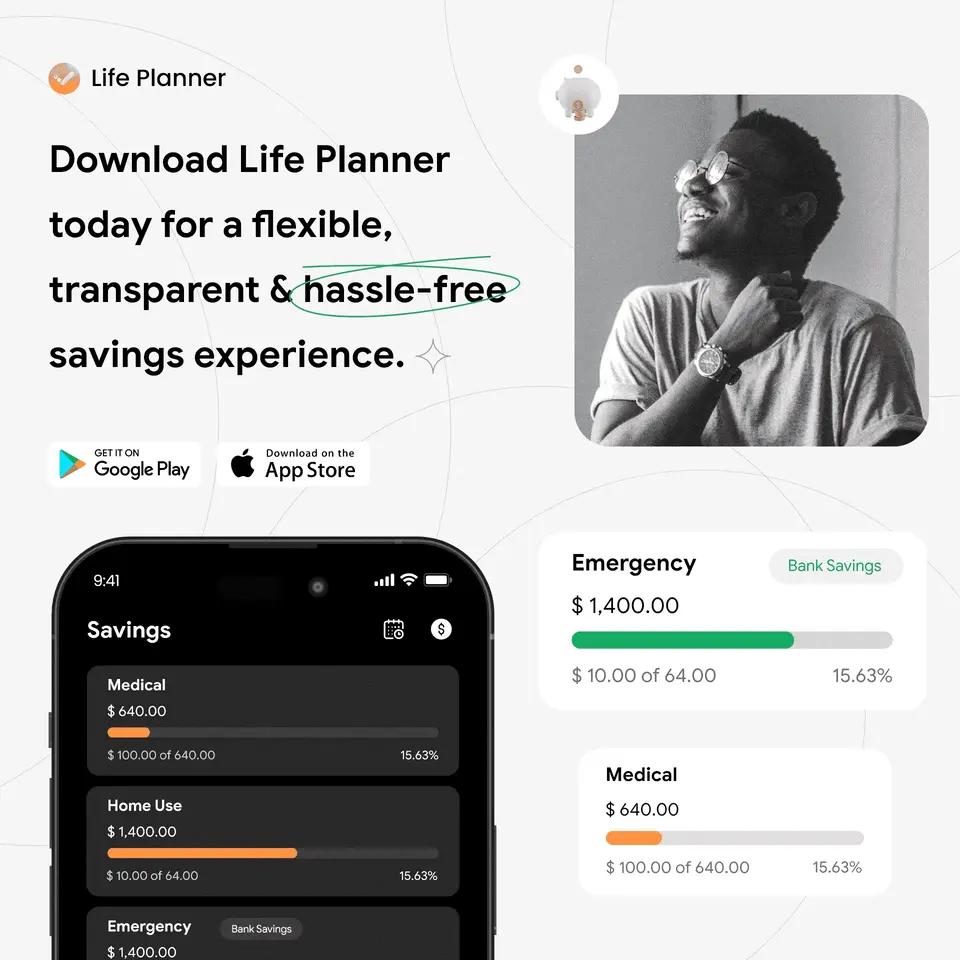

Life Planner

Todo Lists · Habits · Personal Finance · Journal

Ready to get pre-approved the smart way?

Don’t go into your next car purchase blind. Use Life Planner to manage your finances, track pre-approvals, and build the saving habits that lead to better loan terms. Its budgeting and loan tools make comparing lenders effortless, while habit reminders help you stay financially focused all year long.

How to download: Simply tap one of the links below — Google Play or App Store. Then tap Install (Android) or Get (iPhone), open the app, and set up your profile. Once inside, start by adding your pre-approval info to Loan Tracking, set a Savings Goal for your down payment, and schedule reminders in the Habit Tracker to review new loan offers every few weeks.

Should You Finance or Lease Your Next Vehicle?

Car FinanceBuying a new car is exciting — but deciding whether to finance or lease can feel like a puzzle. Each option has perks and tradeoffs that depend on your budget, driving habits, and long-term goals. Let’s break it down in a quick, practical way so you can choose what fits you best.

1. Financing: Ownership with a payoff

Financing means you’re taking out a loan to own the car. You’ll make monthly payments (typically for 36–72 months), and once the loan is paid off, the car is yours. This route usually costs more per month but gives you long-term equity — no mileage limits, no wear-and-tear restrictions, and the freedom to sell anytime.

Use the Life Planner app’s Loan Tracking and Amortization tools to see exactly how much interest you’ll pay, when you’ll own the car outright, and how different loan terms affect your total cost. You can even track lender offers and generate financial reports to stay in full control.

2. Leasing: Lower payments, fewer strings — for now

Leasing is like a long-term rental. You pay to use the car for a few years (often 2–4), then return it or buy it at the end of the lease. Monthly payments are usually lower, but you’ll face mileage caps, potential wear fees, and no ownership at the end — unless you choose to buy.

Leasing can be smart if you like driving newer models or expect your needs to change soon. You can use Life Planner’s Expense Tracker and Budgeting Tools to see how a lease fits into your monthly spending and compare it to financing costs over time.

3. Think lifestyle, not just numbers

Financing suits people who plan to keep their car for years, drive long distances, or want flexibility. Leasing fits those who prefer predictable payments and fresh wheels every few years. But your emotional habits matter too — are you the type who gets attached to your car, or do you crave variety?

The Habit Tracker and Mood Journal in Life Planner can actually help you spot patterns. Track your moods before and after big purchases, or schedule reminders in the Habit Calendar to review financial decisions quarterly. Knowing your behavior makes future choices smoother.

4. The hybrid strategy

Some people lease first, then buy out the car at lease-end if they love it — a “test drive” with an option to own. Use Life Planner’s Savings Goal Tracking to save toward that potential buyout price, while the Budget feature keeps your expenses aligned.

5. The bottom line

Leasing is like borrowing flexibility; financing is investing in ownership. Whichever you choose, keep your total cost of ownership — and your habits — front and center.

The Life Planner app makes this easier with its all-in-one suite: track your auto loan, log payments, manage your budget, and even set habits to improve your financial consistency. It’s personal finance and habit-building rolled into one.

Life Planner

Todo Lists · Habits · Personal Finance · Journal

Should You Finance or Lease Your Next Vehicle?

Car FinanceBuying a new car is exciting — but deciding whether to finance or lease can feel like a puzzle. Each option has perks and tradeoffs that depend on your budget, driving habits, and long-term goals. Let’s break it down in a quick, practical way so you can choose what fits you best.

1. Financing: Ownership with a payoff

Financing means you’re taking out a loan to own the car. You’ll make monthly payments (typically for 36–72 months), and once the loan is paid off, the car is yours. This route usually costs more per month but gives you long-term equity — no mileage limits, no wear-and-tear restrictions, and the freedom to sell anytime.

Use the Life Planner app’s Loan Tracking and Amortization tools to see exactly how much interest you’ll pay, when you’ll own the car outright, and how different loan terms affect your total cost. You can even track lender offers and generate financial reports to stay in full control.

2. Leasing: Lower payments, fewer strings — for now

Leasing is like a long-term rental. You pay to use the car for a few years (often 2–4), then return it or buy it at the end of the lease. Monthly payments are usually lower, but you’ll face mileage caps, potential wear fees, and no ownership at the end — unless you choose to buy.

Leasing can be smart if you like driving newer models or expect your needs to change soon. You can use Life Planner’s Expense Tracker and Budgeting Tools to see how a lease fits into your monthly spending and compare it to financing costs over time.

3. Think lifestyle, not just numbers

Financing suits people who plan to keep their car for years, drive long distances, or want flexibility. Leasing fits those who prefer predictable payments and fresh wheels every few years. But your emotional habits matter too — are you the type who gets attached to your car, or do you crave variety?

The Habit Tracker and Mood Journal in Life Planner can actually help you spot patterns. Track your moods before and after big purchases, or schedule reminders in the Habit Calendar to review financial decisions quarterly. Knowing your behavior makes future choices smoother.

4. The hybrid strategy

Some people lease first, then buy out the car at lease-end if they love it — a “test drive” with an option to own. Use Life Planner’s Savings Goal Tracking to save toward that potential buyout price, while the Budget feature keeps your expenses aligned.

5. The bottom line

Leasing is like borrowing flexibility; financing is investing in ownership. Whichever you choose, keep your total cost of ownership — and your habits — front and center.

The Life Planner app makes this easier with its all-in-one suite: track your auto loan, log payments, manage your budget, and even set habits to improve your financial consistency. It’s personal finance and habit-building rolled into one.

Life Planner

Todo Lists · Habits · Personal Finance · Journal

How to Get the Best Car Loan Deal in 2025

Car LoansHunting for a great car loan in 2025? Interest rates, lender products, and incentives keep shifting — but a smart process will put you in control. Below is a quick, practical playbook you can use right now to secure the lowest overall cost and the best terms for your situation.

1. Know your credit & price range

Your credit score is the single most important factor in the rate you'll be offered. Pull your credit report, check for errors, and aim to improve any quick wins (pay down small balances, correct reporting mistakes) before you lock a loan. Meanwhile, determine what you can comfortably afford by factoring in insurance, fuel, and maintenance — not just the monthly payment.

2. Shop lenders, not just dealers

Dealers can offer attractive promotional rates, but always compare bank, credit union, online lenders, and dealer offers. Get multiple pre-approvals — a pre-approval gives you negotiating power at the dealer and lets you compare apples-to-apples APRs and fees.

3. Focus on the total cost (APR & fees)

Don't be distracted by the lowest monthly payment. Compare APRs, total finance charges, origination fees, and any mandatory add-ons. A longer term lowers monthly payments but increases total interest paid; shorter terms cost more per month but save on interest.

4. Use the down payment to your advantage

A larger down payment lowers the principal, may land you a better rate, and reduces risk of negative equity. If you have a trade-in, get its value separately so you can negotiate the vehicle price and financing independently.

5. Read and negotiate the contract

Ask for the full loan disclosure and amortization schedule. Watch for prepayment penalties, mandatory insurance, or packaged fees. If you see a higher-than-expected rate or hidden fees, negotiate or walk away — plenty of lenders want your business.

6. Consider refinancing later

If rates fall or your credit score improves after purchase, refinancing can reduce your monthly payment or total interest. Keep an eye on market trends (and your own credit) so you can refinance at the right time.

How Life Planner helps you win the loan game

The Life Planner app is a surprisingly powerful ally while shopping for and managing an auto loan. Use its Loan Tracking and Amortization features to upload loan offers, compare amortization schedules, and see exactly how interest and principal change over time. The Expense Tracker and Budgeting Tools help you test different down payment and term scenarios so you can choose what’s sustainable long-term. Set a Savings Goal for a larger down payment and monitor progress in real time.

Build money habits that get you better rates

Lenders look for consistent, reliable behavior. The app’s Habit Tracker and Habit Calendar help you automate saving habits — schedule reminders, track progress, and keep your saving streak. Use the Mood Tracker and Mood Journal when big financial choices feel stressful; spotting mood trends can prevent impulsive decisions at the dealership.

Quick checklist before you sign

- Compare APR, not just monthly payment.

- Get a written pre-approval and an amortization schedule.

- Confirm there are no prepayment penalties.

- Make sure required insurance or add-ons are optional, not mandatory.

- Verify total cost (principal + interest + fees).

Follow these steps and you'll dramatically increase the odds of a great loan outcome — lower interest, fewer surprises, and better control over your finances.

Life Planner

Todo Lists · Habits · Personal Finance · Journal

Ready to take control? Download Life Planner.

Life Planner bundles the tools you need to find, compare, and manage the best car loan for you: loan amortization, lender tracking, budgeting, savings goals, habit-building features, and mood tracking to keep stress in check. It’s designed to make financial decisions clearer and healthier.

How to download: Click the Google Play or App Store link below (or tap the corresponding badge above). That opens the Life Planner store page — press Install (Android) or Get (iOS). After install, open the app, create an account, and start by importing your loan offers into Loan Tracking or setting a Savings Goal. Use Habit Tracker to build a weekly saving routine and the Expense Tracker to confirm affordability.

Get it now: Google Play | App Store

Everything You Need to Know Before Applying for a Loan

Loans & Financial PlanningApplying for a loan can open doors to new opportunities — from buying your dream home to launching a business. But before you sign any paperwork, it’s crucial to understand how loans work, how to prepare, and what lenders really look for. A little planning can save you thousands over time.

1. Know Your Credit and Financial Health

Lenders assess your credit score, income, and debt-to-income ratio to determine if you’re a good candidate. Before applying, review your credit report for accuracy. Use tools like the Life Planner app to monitor your spending through its Expense Tracker and set smart Budget Goals so your finances are in shape.

2. Understand the Loan Types and Terms

Not all loans are created equal. Personal loans, mortgages, and auto loans each have unique terms, interest rates, and repayment schedules. Use Life Planner’s Loan Tracking and Amortization Features to simulate payment plans, compare options, and stay on top of every due date.

3. Calculate What You Can Afford

Borrowing more than you can handle can strain your budget. Before applying, calculate the monthly payments you can realistically afford. With Life Planner’s Financial Reports and Savings Goal Tracker, you can visualize your cash flow and determine how much room you have for a loan payment.

4. Build Healthy Financial Habits

Getting approved for a loan isn’t just about credit — it’s about consistency. The Habit Tracker and Habit Calendar in Life Planner can help you build better saving and payment habits. Schedule reminders, log your progress, and maintain good financial discipline effortlessly.

5. Compare Lenders and Offers

Never accept the first loan offer you receive. Shop around to find better rates, lower fees, or more flexible terms. With Life Planner’s Lender Tracking tools, you can organize details from multiple lenders in one place, making it easy to choose the best deal.

Final Thoughts

Applying for a loan is a major step toward your financial goals — but preparation makes all the difference. With the Life Planner app, you can manage your finances, track your progress, and develop money-smart habits that support your journey.

Ready to take control of your financial future? Download Life Planner today. Simply click your preferred store link below, install the app, and create your first budget or loan plan in minutes. Watch your progress come to life through detailed analytics, habit reminders, and goal tracking tools.

Life Planner

Todo Lists · Habits · Personal Finance · Journal

Top 10 Mistakes to Avoid When Taking Out a Loan

Loans & Money ManagementTaking out a loan can be empowering — whether you’re financing your dream car, a home, or a business venture. But a few common mistakes can turn that opportunity into a financial headache. Let’s break down the top 10 mistakes people make when borrowing — and how you can avoid them using smart planning tools like the Life Planner app.

1. Not Checking Your Credit Score

Your credit score determines the interest rate and loan terms you’ll get. Always check your report before applying. With Life Planner’s Expense Tracker and Financial Reports, you can monitor spending patterns that affect your credit health.

2. Borrowing More Than You Need

It’s tempting to take extra cash “just in case,” but overborrowing increases long-term costs. Use Life Planner’s Budget Tools and Savings Goal Tracker to calculate exactly how much you need.

3. Ignoring the Fine Print

Interest rates, fees, and penalties can hide in the details. Take time to read everything. The Loan Tracking and Amortization Features in Life Planner help you visualize how these terms affect your payments.

4. Focusing Only on Monthly Payments

Low monthly payments can mean longer loan terms and higher interest over time. Track total repayment amounts in Life Planner’s Loan Amortization Tool to see the full picture.

5. Not Comparing Lenders

One lender’s “good offer” might not be the best available. With Life Planner’s Lender Tracking feature, you can compare offers side-by-side to make informed choices.

6. Skipping a Budget Plan

Without a clear budget, loan repayments can sneak up on you. Use Life Planner’s Budget Planner and Expense Tracker to map out how each payment fits into your monthly cash flow.

7. Failing to Build Financial Habits

Responsible borrowing is about consistency. Life Planner’s Habit Tracker, Habit Calendar, and Habit Reminders can help you develop strong repayment and saving routines.

8. Overlooking Emergency Savings

Don’t rely solely on credit for emergencies. Use Life Planner’s Savings Goal Tracking feature to build a safety cushion that keeps you from falling into debt again.

9. Missing Payment Deadlines

Late payments hurt your credit score and cost you in fees. Set up Habit Scheduling and Reminders in Life Planner to ensure you never miss a due date.

10. Not Reviewing Progress Regularly

Loans are long-term commitments. Check your progress often with Life Planner’s Financial Reports and Loan Overview Dashboard to stay motivated and on track.

Final Thoughts

Avoiding these mistakes is all about awareness and organization — and the Life Planner app is designed to make that easy. From budgeting and expense tracking to loan management and habit building, it’s your complete financial assistant in one app.

Ready to take smarter control of your money and make your loan work for you? Download the Life Planner app now. Just click the link for your device below, install the app, and start by setting up your first budget or loan plan. You’ll see your progress unfold through intuitive analytics, reminders, and reports that keep you financially focused and confident.

Life Planner

Todo Lists · Habits · Personal Finance · Journal

How to Improve Your Loan Eligibility Fast

Loans & Credit ImprovementWant to boost your chances of loan approval? Whether you’re eyeing a mortgage, car loan, or personal financing, improving your loan eligibility doesn’t have to take months. With smart strategies, discipline, and the right tools like the Life Planner app, you can elevate your financial profile quickly and confidently.

1. Clean Up Your Credit Report

Start by checking your credit report for any errors or outdated information. Even small mistakes can hurt your score. Track your repayment history and spending habits with Life Planner’s Expense Tracker and Financial Reports to stay on top of your financial reputation.

2. Pay Down Existing Debt

High debt balances reduce your eligibility. Use the Loan Tracking and Amortization Tools in Life Planner to prioritize which loans to pay off first and visualize how every payment improves your creditworthiness.

3. Don’t Miss a Payment

Payment history is one of the biggest factors affecting eligibility. Set automatic Habit Reminders and Payment Schedules in Life Planner to make sure every bill is paid on time — no excuses.

4. Strengthen Your Budget Habits

Lenders love borrowers who manage their money well. Use Life Planner’s Budget and Savings Tools to create a realistic monthly plan. Pair that with the Habit Tracker to build strong budgeting habits over time.

5. Avoid Taking on New Credit Too Soon

Each new credit inquiry can temporarily lower your score. If you’re planning to apply for a loan, hold off on new credit cards or financing. Use Life Planner’s Financial Reports to analyze your readiness and know the best time to apply.

6. Build an Emergency Fund

Lenders view savings as a safety net that reduces risk. With Life Planner’s Savings Goal Tracker, you can set and reach your targets faster — and show lenders that you’re financially responsible.

7. Track and Improve Progress

Monitoring your progress keeps you motivated. The Habit Calendar and Progress Tracker inside Life Planner help you visualize your improvements, so you can see just how far you’ve come.

Final Thoughts

Improving your loan eligibility fast is all about consistency, awareness, and smart financial habits. The Life Planner app combines all the tools you need — from budgeting and loan tracking to habit-building and reminders — so you can stay organized and financially fit.

Ready to take the next step? Download Life Planner today to boost your loan eligibility with ease. Simply click the link for your device below, install the app, and set up your first budget or loan tracker. From there, Life Planner’s built-in analytics, reminders, and goal tracking will guide you toward stronger finances and better loan opportunities.

Life Planner

Todo Lists · Habits · Personal Finance · Journal

Loan Repayment Made Simple: Strategies That Actually Work

Loan Management & Personal FinancePaying off a loan doesn’t have to feel like an endless uphill climb. With the right strategies and a bit of organization, you can simplify your repayment process, stay consistent, and even pay your loan off faster than expected. Here are practical, easy-to-follow strategies — and how the Life Planner app can help make each one easier.

1. Know What You Owe

The first step in simplifying repayment is understanding your loans — how much you owe, your interest rates, and due dates. With Life Planner’s Loan Tracking and Amortization Features, you can visualize your balances, see your progress, and keep all your loan details neatly in one place.

2. Create a Realistic Budget

A solid budget keeps your loan payments consistent and your finances stress-free. Life Planner’s Expense Tracker and Budgeting Tools help you identify where your money goes each month and how much you can safely dedicate toward repayments without cutting corners.

3. Automate Your Payments

Missing a payment can mean late fees and credit score dips. Use Life Planner’s Habit Scheduler and Reminders to stay ahead. Set a recurring habit like “Pay Loan on 15th” — and let the app nudge you when it’s time.

4. Pay More Than the Minimum

Even small extra payments can cut years off your loan term. Track how additional payments impact your loan’s timeline using Life Planner’s Amortization Calculator and see real-time progress toward being debt-free.

5. Use the Snowball or Avalanche Method

Tackle smaller loans first for quick wins (snowball) or focus on high-interest ones (avalanche). Either method works — and with Life Planner’s Financial Reports, you can compare your strategies and celebrate milestones as you go.

6. Build Habits That Support Repayment

Loan repayment success comes down to consistency. Use the Habit Tracker and Habit Calendar in Life Planner to create healthy financial habits, like weekly expense check-ins or monthly savings reviews. Tracking your habits makes progress visible and rewarding.

7. Keep Your Emotions in Check

Staying positive while paying off debt is important. Life Planner’s Mood Tracker and Mood Journal features help you stay mindful and motivated, even when repayment feels slow.

Final Thoughts

Loan repayment doesn’t have to be stressful — it can be a structured, empowering process when you have the right tools. The Life Planner app brings all your financial, habit, and tracking tools into one simple space. You’ll always know what’s due, how you’re progressing, and what to focus on next.

Ready to make your loan repayment journey simple and stress-free? Download Life Planner today. Just click your preferred link below — Google Play or App Store — then install the app. Once it’s on your device, open Life Planner, set up your first loan tracker or repayment habit, and watch how quickly things start to fall into place.

Life Planner

Todo Lists · Habits · Personal Finance · Journal

Loan Calculators Explained: How to Estimate Your Monthly EMI

Loan Planning & Financial ToolsThinking about taking a loan but unsure how much you’ll need to pay each month? That’s where loan calculators come in! A loan calculator helps you estimate your EMI (Equated Monthly Installment) — the fixed amount you’ll pay every month to clear your loan, including both principal and interest. Let’s break down how it works and how the Life Planner app can make loan planning effortless.

1. The EMI Formula (Made Simple)

EMI is calculated based on three factors — the loan amount, the interest rate, and the tenure. Most loan calculators, like the one built into the Life Planner app, use the formula:

EMI = [P x R x (1+R)^N] / [(1+R)^N – 1]

where P is the principal loan amount, R is the monthly interest rate, and N is the total number of months.

2. Why Use a Loan Calculator?

Instead of guessing your payments, a calculator gives you accurate figures instantly. It helps you compare loan offers, plan your finances, and avoid surprises. With Life Planner’s Loan Tracking and Amortization Tools, you can simulate various scenarios — from changing interest rates to adjusting tenure — and see how they affect your EMI.

3. Plan Your Budget Around Your EMI

Once you know your EMI, the next step is making sure it fits your budget. The Expense Tracker and Budgeting Tools in Life Planner let you align your monthly spending and savings goals with your repayment schedule. You can even set up Habit Reminders to ensure you never miss a payment.

4. Stay on Track with Financial Discipline

Repaying a loan on time requires consistency. That’s where Life Planner’s Habit Tracker and Habit Calendar shine — helping you build and maintain money-smart habits like saving, tracking expenses, and reviewing financial goals regularly.

5. Visualize Your Progress

Numbers can get overwhelming, but visuals make it simple. Life Planner’s Financial Reports and Loan Overview Dashboards show your progress in clear graphs and summaries, so you can celebrate how much you’ve paid and how close you are to being debt-free.

Final Thoughts

Understanding your loan and EMI is the first step toward stress-free borrowing. With the Life Planner app, you get more than just a loan calculator — you get an all-in-one financial assistant that helps you track, plan, and manage your loans while building strong financial habits.

Ready to take control of your finances? Download Life Planner today. Just click your preferred link below, install the app, and open it on your phone. From there, go to the Loan Tracking section, enter your loan details, and watch your EMI and repayment schedule come to life — simple, clear, and empowering.

Life Planner

Todo Lists · Habits · Personal Finance · Journal

Home Loan 101: A Beginner’s Guide to Buying Your First House

Home Loans & Financial PlanningBuying your first home is a huge milestone — exciting, a little intimidating, and definitely full of numbers. Understanding how home loans work is the first step to turning your dream home into reality. Whether you’re browsing listings or planning your down payment, here’s a simple guide to get you started — with a little help from the Life Planner app to make the process stress-free.

1. Understand What a Home Loan Is

A home loan lets you borrow money from a bank or lender to buy property, and you pay it back in monthly installments over several years. Sounds simple enough — but the key is in knowing your interest rates, tenure, and repayment terms. The Loan Tracking and Amortization Features in Life Planner help you visualize your total repayment and how much of each payment goes toward interest and principal.

2. Check Your Credit Score

Your credit score determines your loan eligibility and interest rate. Before applying, review your score and identify areas to improve. The Expense Tracker and Budget Tools in Life Planner help you manage payments, avoid missed bills, and keep your credit healthy.

3. Set a Realistic Budget

Don’t just plan for the house price — consider property taxes, insurance, maintenance, and closing costs. Use Life Planner’s Budgeting and Financial Reports to get a full view of what you can afford without overextending yourself.

4. Save for the Down Payment

Most lenders require a down payment of at least 10–20%. Start saving early using Life Planner’s Savings Goal Tracker. You can set targets, track progress, and even schedule Habit Reminders to make regular contributions toward your home fund.

5. Compare Lenders and Loan Offers

Don’t settle for the first offer you see. Compare interest rates, fees, and flexibility. Life Planner’s Lender Tracking tool helps you organize and compare loan options side by side — so you always pick the smartest deal.

6. Stay Consistent With Your Finances

Once you have your loan, consistency is key. The Habit Tracker and Habit Calendar in Life Planner can help you build solid repayment habits and monitor your progress month after month. Small, steady actions make a big difference in staying on track.

Final Thoughts

Buying your first home doesn’t have to be overwhelming. With the right preparation and tools, you can make confident decisions every step of the way. The Life Planner app gives you everything you need — from budgeting and saving to loan tracking and habit-building — all in one place.

Ready to start your journey toward homeownership with confidence? Download Life Planner today. Simply click your preferred link below to install it from Google Play or the App Store. Once installed, open the app, set up your first savings goal or loan plan, and let Life Planner guide you — step by step — toward your dream home.

Life Planner

Todo Lists · Habits · Personal Finance · Journal

Fixed vs. Floating Interest Rates — Which Home Loan Is Right for You?

Home Loans & Financial PlanningChoosing between a fixed and floating interest rate can feel like standing at a financial crossroads. Both come with their perks — and their pitfalls. The key is understanding how each works and which one suits your financial style. Let’s break it down simply so you can make an informed choice — with a little help from the Life Planner app to keep your finances steady and stress-free.

1. What Is a Fixed Interest Rate?

A fixed interest rate stays the same throughout your loan term. That means your monthly EMI (Equated Monthly Installment) won’t change — even if market rates rise or fall. It’s predictable, simple, and perfect for those who love stability. Using the Loan Tracking and Amortization Tools in Life Planner, you can clearly see how much of your payment goes toward interest versus principal, making financial planning easier.

2. What Is a Floating Interest Rate?

Floating rates change based on market conditions. When interest rates drop, you’ll pay less; when they rise, your EMI goes up. It’s great for risk-takers and those expecting rates to fall over time. To stay on top of these changes, Life Planner’s Financial Reports and Lender Tracking features can help you monitor trends and adjust your budget accordingly.

3. The Pros and Cons

Fixed Rate: Stability, easy budgeting, but slightly higher starting rates.

Floating Rate: Potentially lower long-term costs, but unpredictable monthly payments.

With Life Planner’s Budgeting Tools and Expense Tracker, you can simulate both scenarios — seeing how each option fits your monthly income and financial habits before committing.

4. Choosing What’s Best for You

If you prefer consistency and peace of mind, a fixed rate might be your best friend. If you’re comfortable with some variability and want to save when rates dip, floating is worth the gamble. Use Life Planner’s Savings Goal Tracker and Habit Scheduler to stay disciplined — saving a little extra each month as a cushion for possible EMI increases.

Final Thoughts

Whether you go fixed or floating, the best choice is the one that matches your financial goals and personality. The Life Planner app makes it easy to plan, track, and manage every step — from setting your loan goals to reviewing amortizations and keeping your budget in check.

Ready to take control of your home loan journey? Download Life Planner today and turn financial planning into a habit. Click your preferred link to install it from Google Play or the App Store. Once installed, open the app, create your first loan plan or financial goal, and let Life Planner guide you toward smarter, stress-free homeownership.

Life Planner

Todo Lists · Habits · Personal Finance · Journal

Top Banks Offering the Lowest Home Loan Rates in 2025

Home Loan RatesLooking for the lowest home loan rates this year? Instead of a fixed list of banks (which can change weekly), here’s a practical, trustworthy approach to finding the best lenders and rates in 2025 — plus how to use the Life Planner app to compare and plan like a pro.

1. Where to Look for Current Lowest Rates

Interest rates change often. Check official bank websites, central bank updates, and reputable financial comparison sites for up-to-date rate tables. Also ask your local branch about any special offers or rate discounts for salary account holders, first-time buyers, or specific professions.

2. How to Compare Offers Easily

Don’t focus only on the headline rate. Compare the annual percentage rate (APR), processing fees, prepayment penalties, and whether the rate is fixed or floating. Use Life Planner’s Lender Tracking and Loan Amortization tools to log offers, simulate EMIs, and see the true cost over time.

3. Watch Out for Hidden Costs

A seemingly low interest rate can be offset by high setup fees, insurance, or early repayment charges. Life Planner’s Financial Reports and Expense Tracker help you factor all costs into your monthly budget so you won’t be surprised later.

4. Use Your Credit & Savings to Negotiate

A strong credit score, stable income, and a larger down payment usually translate to better rates. Track and improve these with Life Planner’s Budgeting Tools, Savings Goal Tracker, and Habit Tracker — show lenders you’re low-risk and more likely to qualify for discounts.

5. Timing & Type Matter

Market cycles and central bank decisions affect floating rates; promotions affect fixed-rate deals. Decide whether you need the predictability of a fixed rate or the potential savings of a floating rate, then model both scenarios in Life Planner’s Loan Tracking and Amortization views.

6. Local vs. National Lenders

Local banks and credit unions sometimes offer competitive niche deals, while national banks can offer scale advantages. Keep a short list (use Life Planner’s Lender Tracking) and compare actual offers rather than relying on reputation alone.

Practical Checklist Before You Apply

- Verify current published rates on official lender sites.

- Check APR, fees, and penalties — not just the headline rate.

- Simulate EMIs and total interest using an amortization tool.

- Ensure your budget can absorb the EMI — use Life Planner’s Budget Planner.

- Keep an emergency fund tracked in Life Planner’s Savings Goals.

Final Thoughts

Rather than memorizing a list of banks (which can quickly go out of date), build a process: research current published rates, compare true costs, and model outcomes. With the Life Planner app, you can store lender offers, run amortization scenarios, track budgets and savings, and build habits that improve your borrowing profile.

Ready to compare, plan, and lock in the best possible home loan for you? Download Life Planner now. Click the link for your device — Google Play or App Store — then install the app. After installation: open Life Planner, create your financial profile, add lender offers into the Lender Tracking section, and use the Loan Amortization tool to compare real monthly costs. Use Habit Tracker and Habit Reminders to build consistent saving and payment routines — small habits that make big rate differences over time.

Life Planner

Todo Lists · Habits · Personal Finance · Journal

Step-by-Step Guide to Refinancing Your Home Loan

Home Loan RefinancingRefinancing your home loan can feel like a big decision — but with the right plan, it can save you thousands in interest and help you reach financial freedom faster. Whether you’re looking for a lower rate, shorter term, or simply more flexibility, this step-by-step guide will walk you through the refinancing process with confidence.

Step 1: Know Why You’re Refinancing

Are you hoping to reduce your monthly payments, shorten your loan term, or access your home equity? Knowing your “why” helps you pick the right refinancing type. The Life Planner app can help you visualize your financial goals with its Budgeting Tools and Savings Goal Tracker, ensuring you make choices that align with your bigger picture.

Step 2: Check Your Current Loan Details

Review your existing interest rate, remaining balance, and remaining term. Use Life Planner’s Loan Tracking and Amortization Features to get a clear snapshot of where you stand and how refinancing might affect your total cost and timeline.

Step 3: Compare Lenders and Rates

Shop around! Compare fixed and floating rate offers from banks and financial institutions. Life Planner’s Lender Tracking tool allows you to log and compare offers, while its Financial Reports help you analyze your savings over time.

Step 4: Calculate Your Break-Even Point

Refinancing isn’t free — there are fees involved. The key is to determine when your savings will outweigh your costs. You can model this in Life Planner’s Amortization Calculator to see how soon you’ll start saving money after switching loans.

Step 5: Prepare Your Documents

You’ll typically need income proof, tax returns, and details of your existing loan. Create a checklist in Life Planner’s To-Do List section so you don’t miss a thing during the process.

Step 6: Apply and Lock Your Rate

Once you’ve chosen your lender, submit your application and lock in your interest rate. Use Life Planner’s Habit Reminders to track important follow-up dates or payment transitions to stay organized through every step.

Step 7: Track and Maintain Your New Loan

Once your refinancing is approved, monitor your payments regularly. Life Planner’s Loan Tracking and Expense Tracker help ensure you stay on top of your finances — no surprises, no stress.

Bonus Tip: Build Better Financial Habits

Refinancing is a financial reset — take advantage of it! Use Life Planner’s Habit Tracker and Habit Calendar to stay consistent with saving, budgeting, and on-time payments. Over time, these habits make managing your loan effortless.

Ready to Take the Next Step?

Refinancing can be your smartest financial move of 2025 — and with Life Planner, you can make it smooth, strategic, and stress-free. Download the app today on Google Play or the App Store. Simply click your preferred link, install the app, and start by adding your current loan details under “Loan Tracking.” Then, set your refinancing goals, compare lender offers, and let Life Planner’s analytics and reminders guide your journey to lower payments and better habits.

Life Planner

Todo Lists · Habits · Personal Finance · Journal

Hidden Costs in Home Loans No One Tells You About

Home LoansBuying a home is one of life’s biggest milestones — and for most of us, that means taking on a home loan. But while you might focus on the interest rate and EMI, there are a few *hidden costs* that can sneak up on you. These are the quiet charges that banks often don’t highlight upfront, yet they can add thousands to your total expense.

1. Processing Fees

Most lenders charge a processing fee — usually between 0.5% and 2% of the loan amount — just to review your application. Even if your loan doesn’t get approved, you might not get that fee refunded. You can use the Life Planner app’s Expense Tracker to log and categorize these one-time costs so they don’t get lost in the shuffle.

2. Legal and Technical Evaluation Charges

Before approving your loan, the bank may conduct property verification and valuation. These charges are often separate from your main loan costs. Tracking these with Life Planner’s Budgeting Tools ensures you stay within your budget while managing all the fine print.

3. Prepayment and Foreclosure Penalties

Planning to repay your loan early? Some banks charge penalties for prepayments or foreclosures. Use Life Planner’s Loan Tracking and Amortization Features to simulate different payment timelines and see if prepaying makes financial sense for you.

4. Late Payment Charges

Even one missed EMI can invite hefty late fees. Avoid them altogether with Life Planner’s Habit Reminders and Payment Scheduling — your personal assistant for staying on top of every due date.

5. Conversion Fees for Lower Rates

If your bank offers to switch you from a fixed to a floating rate (or vice versa), there’s often a conversion charge. These can range from a few thousand to a percentage of your outstanding loan amount. Use Life Planner’s Financial Reports to calculate if the switch is truly worth it.

6. Insurance and Documentation Costs

Many lenders bundle home insurance with your loan — sometimes without clarifying that it’s optional. Always read the fine print and keep copies of every fee in Life Planner’s Journal or Expense Tracker to avoid paying for what you don’t need.

Final Thought

Hidden costs don’t have to catch you off guard. With the right planning and tracking tools, you can keep every rupee accounted for. The Life Planner app helps you manage loans, budgets, and habits — all in one place — so you stay in control of your finances, not the other way around.

Ready to take charge of your home loan journey? Download Life Planner today on Google Play or the App Store. Simply click your preferred link, install the app, and start by adding your current home loan details under “Loan Tracking.” Then use its Expense Tracker and Financial Reports to uncover every hidden cost and plan smarter for your future home investments.

Life Planner

Todo Lists · Habits · Personal Finance · Journal